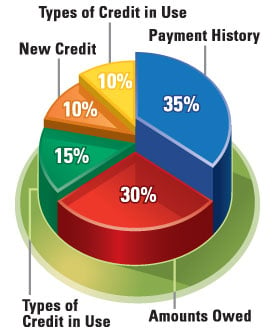

If you’re thinking of purchasing a Wilmington area home, then your first step should be to pull your credit reports, in particular your FICO® Score, which is checked by most major lenders. It will give you a fair idea of how likely you are to get a loan with a good interest rate. Your FICO® Score is a number between 300 and 850 that is calculated based on your payment history, outstanding balances, length of credit history, new credit, and types of credit. The higher the number, the less of a risk lenders will see you as. So, it’s important to raise your score as high as possible before applying for a loan.

At MyFico.com, you can check your FICO® Score and credit reports. You’ll be able to see your credit accounts, payment history, who has accessed your credit reports, and any public record items, like bankruptcies, liens, judgments, etc. Most importantly, pulling your credit reports will show you if there are any mistakes that may potentially hurt your chances at getting a loan.

If you do find errors in your credit reports, contact the credit reporting agencies directly:

| Equifax (800) 685-1111 www.equifax.com |

Experian (888) 397-3742 www.experian.com |

Trans Union (800) 916-8800 www.transunion.com |

If you find your score is less than stellar, there are a few steps that you can take to raise your credit:

- Pay your bills on time. The easiest solution is setting up auto-payments, but you may not feel comfortable doing that. Web sites like Mint.com will notify you when it’s time to pay a bill. You just need to plug-in some info and you’ll get either an email or a phone notification. It also has some other tools for tracking your spending and saving you money. It’s definitely a tool you should check out.

- Pay down debt. Start with the credit lines that are closest to being maxed out, because they pop up as red flags to lenders. But don’t close unused credit lines. It looks better to have available credit than none at all. If you don’t have a credit history, you should apply for a few lines of credit (gas cards, department store cards, credit cards, etc.), but not all at once as multiple credit inquiries can lower your score. Instead, allow three months between applications. Then, use those cards a few times to create a history, but keep the balances low.

- Correct any errors. As stated above, these can lower your score.

- Meet with a lender. We know a few lenders that will happily sit down with you, take a look at your history, and give specific suggestions that will help you get your score in better standing. Feel free to give us a call (910.202.2546) or send us a message through our Contact page and we’ll give you a referral.

Taking the time to get your credit squared away prior to applying for a home loan could save you thousands of dollars over time. Make sure you pull your reports even if you feel confident that your scores are high. It’s better to be 100% sure before you agree to the mortgage terms. You could be getting better.