If you’re in the market to buy a home—especially in competitive real estate markets like Wilmington, Leland, or anywhere in coastal North Carolina—you’ve probably heard the term “earnest money” come up. For first-time buyers or even seasoned homeowners, the earnest money deposit can be a bit of a mystery. How much should you offer? Is it refundable? And more importantly, how do you make sure you don’t lose it?

This guide will walk you through the ins and outs of earnest money, from what it is and why it exists, to how it works in a real estate transaction, and what you can do to protect your deposit. Whether you’re buying a home in New Hanover County, eyeing a lot in Brunswick County, or making moves anywhere else in North Carolina, understanding earnest money is crucial to navigating the home-buying process with confidence.

What Is Earnest Money?

At its core, earnest money is a good faith deposit that a buyer makes to show they’re serious about purchasing a home. Think of it as putting skin in the game. It’s not required by law in every state, but it’s standard practice in many competitive markets—and especially common in North Carolina.

When you make an offer on a home, your earnest money is typically submitted along with the offer or shortly thereafter. If the seller accepts your offer, that money is then held in an escrow account (usually by the listing firm, buyer’s agent’s firm, or a closing attorney) until closing.

Home Buyer Smiling at New Home

Earnest Money vs. Due Diligence Fee (in North Carolina)

If you’re buying in North Carolina, you’ll also hear about the due diligence fee, which is separate from earnest money. The due diligence fee is a non-refundable payment made directly to the seller and is immediately theirs to keep. In contrast, earnest money is generally refundable if the buyer backs out of the deal for a reason permitted in the contract.

In most North Carolina real estate transactions, you’ll provide both a due diligence fee and an earnest money deposit. They serve slightly different purposes, but both contribute to the overall seriousness of your offer.

How Much Earnest Money Should You Offer?

The amount of earnest money can vary based on a few factors, including the market you’re buying in, how competitive it is, and the purchase price of the home. Here’s a general breakdown to guide you:

National Guidelines

-

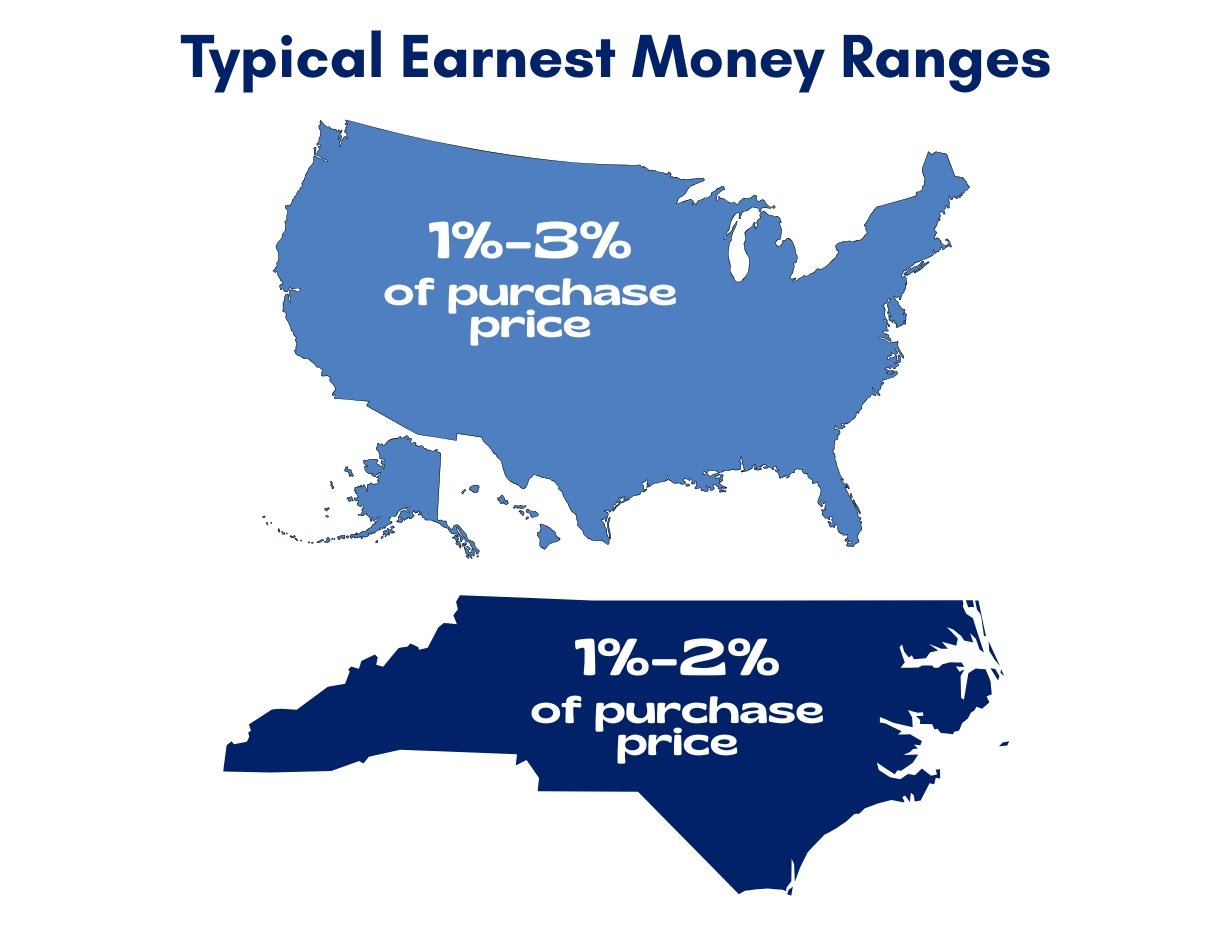

Typical earnest money amounts range from 1% to 3% of the purchase price of the home.

-

In a buyer’s market, 1% might be perfectly acceptable.

-

In a seller’s market—especially in hot areas like Leland, Carolina Beach, or Wilmington—it’s not uncommon for earnest money to be closer to 2-3% (or even higher) to show commitment.

North Carolina Considerations

In North Carolina, buyers often provide:

-

A due diligence fee (ranging from a few hundred dollars to several thousand, depending on the home’s value and competitiveness)

-

An earnest money deposit (1%–2% of the sale price is typical, but this is negotiable)

Let’s say you’re buying a $450,000 home in Brunswick Forest. A typical earnest money deposit might range from $4,500 to $9,000. Combine that with a due diligence fee of $1,000–$2,000, and you’re looking at several thousand dollars upfront—before you even get the keys.

What Happens to the Earnest Money?

Once you go under contract, your earnest money is held in an escrow account by an independent third party, such as a real estate firm or closing attorney. It’s not immediately given to the seller, and it’s not lost money—as long as everything goes according to plan.

At closing, the earnest money is applied toward your:

-

Down payment

-

Closing costs

-

Or any other applicable transaction costs

So, in the best-case scenario, earnest money is essentially a prepayment toward your overall purchase. However, if things don’t go as planned, the rules about what happens to it depend on why the deal falls apart.

When Do You Risk Losing It?

This is the part that makes some buyers nervous—and understandably so. You can lose your earnest money under certain circumstances, especially if you don’t terminate the contract properly or within the timelines agreed upon.

Here are a few situations where a buyer could forfeit their earnest money:

1. Backing Out After Due Diligence Ends

In North Carolina, the due diligence period is your window to investigate the home. This is when you do your inspections, secure financing, get the appraisal, and make sure the title is clear.

If you decide to back out of the deal after the due diligence period has ended—and for a reason not protected by the contract—you’ll likely lose your earnest money (and already paid due diligence fee, which is non-refundable).

2. Missing Contract Deadlines

Time is of the essence in real estate. If you fail to meet key deadlines—like securing your loan or making repair requests—you could be considered in breach of contract and risk losing your deposit.

3. Defaulting on the Contract

If you break the terms of the purchase agreement (for example, by not showing up to closing), the seller may be entitled to keep your earnest money as damages.

How Buyers Can Protect Their Earnest Money

The good news? With a little planning and some expert guidance, you can avoid losing your earnest money. Here’s how to safeguard your deposit throughout the process:

1. Work with an Experienced Real Estate Agent

An experienced agent (like those on our team here at The Cameron Team) will help you structure your offer in a way that protects your interests. We’ll walk you through every contingency, explain your deadlines, and make sure your earnest money is properly handled.

2. Negotiate a Reasonable Due Diligence Period

Make sure your due diligence period gives you enough time to:

-

Schedule inspections

-

Get your financing in order

-

Review the property’s history and disclosures

-

Secure an appraisal

If your due diligence window is too short, you might be forced to make decisions under pressure or miss key deadlines, risking your deposit.

3. Understand the Contract Terms

Before you sign, make sure you clearly understand what contingencies exist and what happens if you need to walk away from the deal. Your agent and closing attorney can explain these details and help you stay compliant.

4. Keep Documentation

Save all communication with your lender, inspectors, and the seller’s agent. If any dispute arises, having a record can help prove that you acted in good faith and within the terms of the contract.

Don’t Skip the Home Inspection

5. Don’t Skip the Home Inspection

Even if you’re tempted to waive the inspection to make your offer more competitive, that can be a costly mistake. A home inspection can uncover issues that may allow you to renegotiate or back out within the due diligence period—without losing your earnest money.

Should You Offer More to Strengthen Your Offer?

In a hot market, sometimes offering a larger earnest money deposit can make your offer stand out. Sellers love seeing a serious buyer who’s willing to put more money on the line—it signals confidence and commitment.

However, before increasing your earnest money deposit:

-

Talk with your real estate agent about what’s typical for the neighborhood or community.

-

Make sure you’re financially comfortable with the amount.

-

Ensure you have your financing lined up and understand the risks involved.

Final Thoughts: Earnest Money as a Tool, Not a Trap

Earnest money isn’t something to fear—it’s a tool that helps both buyers and sellers feel confident in a real estate transaction. For sellers, it shows the buyer is serious. For buyers, it signals to the seller that you mean business and helps solidify your offer.

That said, it’s essential to know the rules, timelines, and protections in your contract. With the right guidance from a professional real estate agent, you can use earnest money strategically—without putting your investment at unnecessary risk.

If you’re ready to start your home-buying journey in the Wilmington area, including Leland, Hampstead, Carolina Beach, or beyond, our experienced team at The Cameron Team is here to help you navigate every step of the process—including how to craft a competitive offer with earnest money that works for you.

Need help buying a home in Southeastern North Carolina?

Reach out to The Cameron Team today—we’ll make sure your earnest money (and your future home) is in good hands. 🏡