Real estate transactions can be complex, but when you throw a tropical storm or hurricane into the mix, things get even more complicated. Let’s dive into the various ways these weather events can impact a real estate closing and what you can do to navigate the stormy waters.

Insurance Moratoriums on Binding Coverage

One of the first hurdles you’ll encounter is an insurance moratorium. When a tropical storm or hurricane is on the horizon, insurance companies often place a moratorium on binding new coverage. Essentially, they put a “box” around the storm, halting the issuance of new policies not just in the direct path but also in surrounding areas that could potentially be affected by the storm’s impact. This box is an area defined by the insurance company that includes a wide perimeter around the predicted path of the storm. Properties within this box, even if they aren’t directly in the storm’s path, cannot obtain new insurance coverage until the threat passes.

This precautionary measure means you can’t secure the necessary homeowner’s insurance required by lenders to close the deal. Without insurance, lenders won’t proceed with the closing, putting your scheduled closing date on hold. It’s crucial to stay in constant communication with your insurance agent and keep an eye on weather reports. As soon as the moratorium lifts, be ready to bind coverage immediately to minimize delays. Understanding the breadth of these moratoriums and planning accordingly can help mitigate their impact on your closing process.

Postponed Inspections and Negotiated Repairs

Inspections are a key part of the closing process, but when a storm is brewing, they can be postponed. Likewise, any negotiated repairs may also be delayed. This can lead to frustration and uncertainty for both buyers and sellers. If the property sustains damage during the storm, new negotiations for repairs will be necessary, potentially altering the terms of your agreement. To mitigate these issues, schedule inspections as early as possible to avoid conflicts with impending weather and ensure all parties understand the implications of any delays.

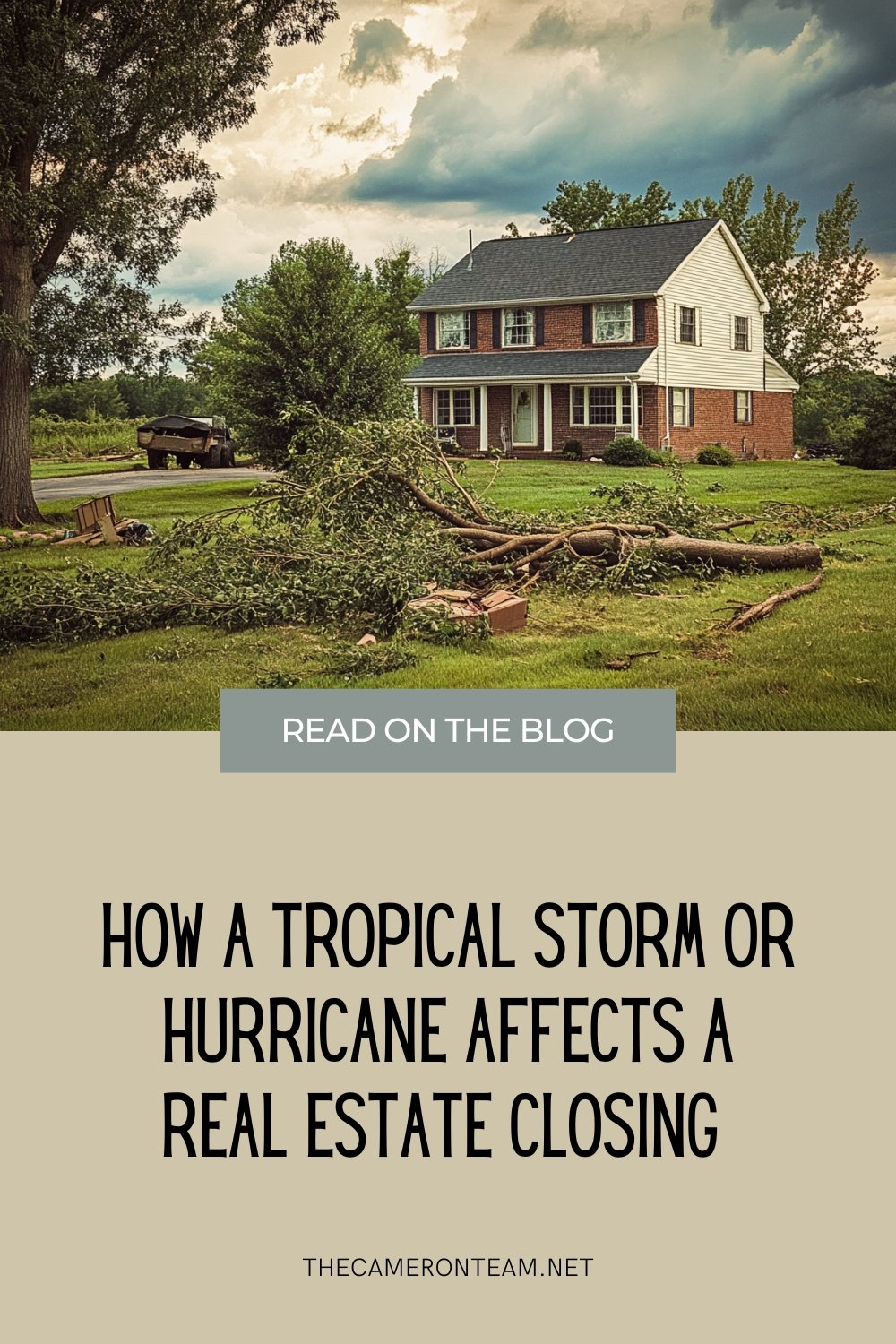

Storm Debris

Potential Damage to the Property

If the storm causes damage to the property, sellers are typically responsible for repairs. However, this can complicate the closing process significantly. Significant damage may require extensive repairs, pushing back the closing date and potentially affecting the property’s appraised value, which can impact your loan approval. To avoid disputes and ensure smooth handling of such situations, have a clear clause in your contract regarding repairs and responsibilities.

Potential Reinspections Requested by Lenders

After a storm, lenders often require a reinspection by an appraiser to ensure the property is still in acceptable condition. Scheduling a reinspection can take time, especially if appraisers are dealing with a backlog of requests. Moreover, reinspection fees may add to your closing costs, adding another layer of complexity. To expedite reinspections, work closely with your lender and real estate agent to stay ahead of the curve and minimize delays.

Post-Storm Backlog for Servicers and Attorneys

A major storm can overwhelm local servicers and attorneys, leading to a backlog of work. This backlog can result in extended timelines for document processing and title searches. Additionally, it might be harder to get appointments with attorneys and other essential parties, further delaying the closing process. To keep the process moving as smoothly as possible, be patient and maintain open communication with all parties involved. Understanding the potential for delays and setting realistic expectations can help manage stress and ensure a smoother transaction.

Post-Storm

Navigating the Stormy Waters

Navigating a real estate closing during or after a tropical storm or hurricane requires patience, preparation, and clear communication. Staying informed is key. Keep a close eye on weather reports and stay in touch with your real estate agent, lender, and insurance agent. Be flexible and understand that delays are common, so be prepared to adjust your plans accordingly. Regular updates with all parties involved can help manage expectations and keep the process on track.

By understanding these challenges and preparing for them, you can successfully navigate the complexities of closing a real estate transaction during or after a tropical storm or hurricane.

FAQs

Q: Can I still close on a property if there’s a hurricane warning?

A: It depends on various factors, including insurance moratoriums and property condition. Communicate with your lender and real estate agent for guidance.

Q: Who is responsible for repairing storm damage to the property?

A: Typically, the seller is responsible for repairing any storm damage before closing, but it’s essential to have this clearly outlined in your contract.

Q: How long can an insurance moratorium last?

A: It varies by insurer and the severity of the storm, but moratoriums generally lift once the immediate threat has passed.

Q: What should I do if the property is significantly damaged during a storm?

A: Contact your real estate agent and attorney to discuss your options, which may include renegotiating the terms or even postponing the closing.

By staying proactive and informed, you can ensure your real estate closing remains as smooth as possible, even in the face of a tropical storm or hurricane.

How a Tropical Storm or Hurricane Affects a Real Estate Closing