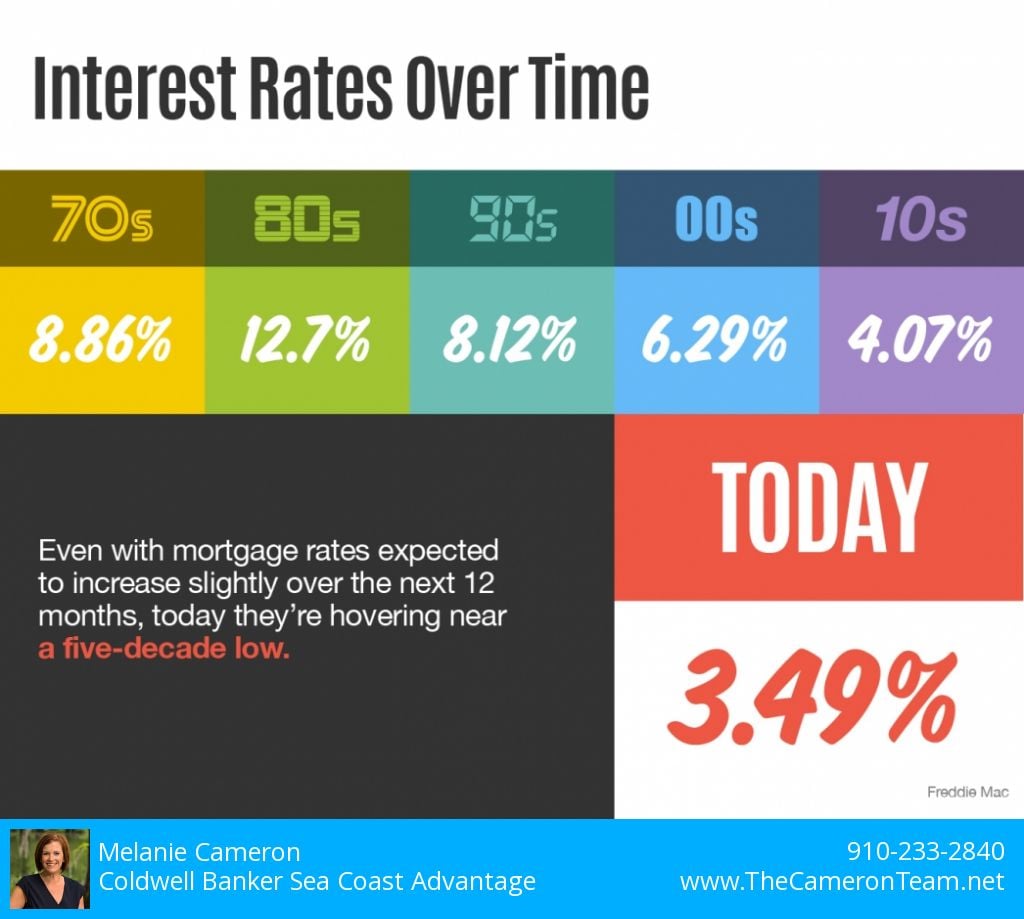

A tight inventory and buyer demand has led to an increase in home values. The typical home in the United States now costs $244,054. That is 3.7% higher than December 2018, according to a report from Zillow. When potential buyers see prices rise, it’s a gut reaction to think that homes are less affordable, and they should hold off on purchasing a property. But that’s a common misconception. Interest rates play a significant role in the affordability of homes and they are at the lowest they’ve been in five decades.

Matter-of-fact, as pointed out by Black Knight, a leading provider of data and analytics solutions, in their Mortgage Monitor, “Despite the average home price increasing by nearly $13,000 from just over a year ago, the monthly mortgage payment required to buy that same home has actually dropped by 10% over that same span due to falling interest rates.” Buyers can now purchase a more expensive home while paying the same principal and interest. It equates to a roughly 16% increase in buying power.

Of course, buying power does have a cap that’s determined by the consumer’s finances and the state of their local real estate market, but an increase in values does not equate to less affordability. If the interest rates rise as home prices do, then owning a home can become less affordable. But, right now, interest rates remain low.

Another factor in home affordability is the buyer’s income. The average household income has risen 5% since last year. The average income of a person in Wilmington, NC, is $29,225. A 5% increase from that is $1,461.25. That’s a whole mortgage payment.

Keep in mind, as real estate market inventory has fallen, rental prices have risen. It’s the classic case of supply-and-demand. While this is great for investors, it’s made it increasingly harder for people to find homes to rent at an affordable price. In many cases, if you can buy a home instead of rent, that will be more beneficial to you. It doesn’t matter if you’re a renter or owner, your money is going towards a mortgage. At least when you buy, it’s your mortgage, your equity, and your wealth.

The best way to determine if buying a new home is an option for you is to speak with a mortgage broker or lender. They can give you the most accurate and up-to-date information taking into account your personal finances, current rates, and available loan packages. We always recommend using a local mortgage professional. If you’re considering buying in the Wilmington area, let us know. We’re happy to give you a few names of mortgage brokers we’ve had good experiences with in the past.

[the_grid name=”Home Buyer Tips”]