When you inherit a property, amidst the emotional journey of losing a loved one, you’re suddenly thrust into the world of tax implications, wondering, “Do I owe Uncle Sam a piece of this?” The answer isn’t as straightforward as you might hope, but we’re here to clear the fog and offer clarity. The world of taxes can feel like a labyrinth, but understanding capital gains tax on inherited property is crucial to navigating it successfully.

Capital Gains Tax: The Basics

First off, let’s break down what capital gains tax is. In essence, it’s the tax you pay on the profit from selling an asset, like property, stocks, or bonds, that has increased in value over time. The key here is the “increase in value.” If you sell something for more than what it cost you, that profit is what’s taxed. However, inherited property throws a unique curveball into this equation.

Stepped-Up Basis: The Game Changer

Here’s where it gets interesting for inherited properties. Typically, when you inherit property, you benefit from something called a “stepped-up basis.” This means the property’s tax basis is “stepped up” to its market value at the time of the deceased’s death. Why does this matter? Because if you sell the property, the capital gains tax you might owe is based on any increase in value from the time you inherited it, not from what the original owner paid. This can significantly reduce the capital gains tax you owe if the property has appreciated over the years.

When Do You Pay Capital Gains Tax on Inherited Property?

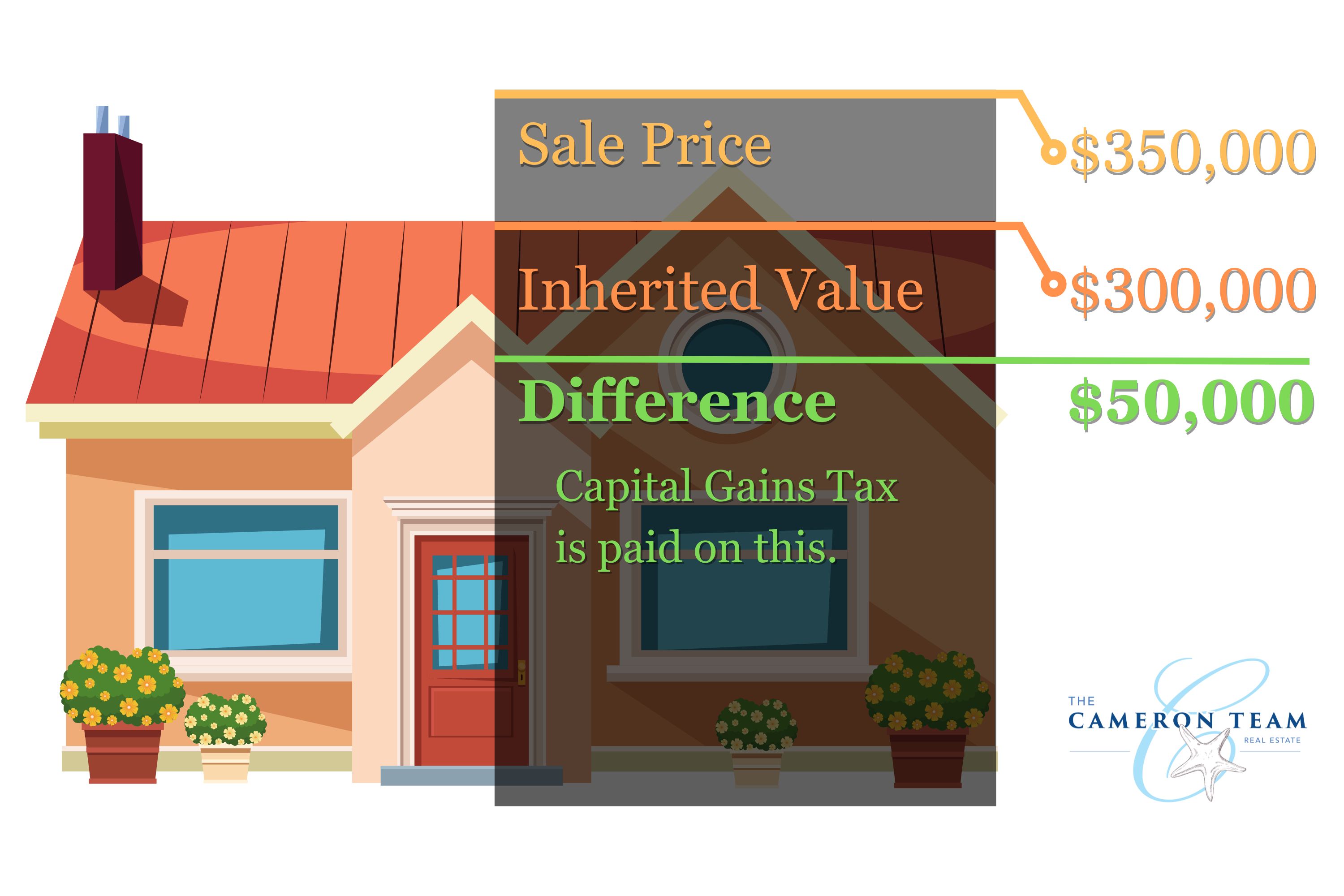

So, do you pay capital gains tax on inherited property? Yes, but only if you sell the property and it has increased in value since you inherited it. Here’s a simplified example: Imagine you inherited a house that was valued at $300,000 when you received it, and you later sell it for $350,000. The $50,000 profit is what you could owe capital gains tax on, not the full $350,000.

Capital Gains Tax Paid on Inherited Property

See current Capital Gains Tax rates.

Exclusions and Exceptions

It’s not all about paying out; there are exclusions and exceptions that can work in your favor. For instance, if you decide to live in the inherited property as your primary residence for at least two years, you may qualify for an exclusion that allows you to exclude up to $250,000 (or $500,000 for married couples) of the gain from your income. It’s nuances like these that can make a significant difference in your tax responsibilities.

Navigating the Tax Waters

Understanding and calculating capital gains tax on inherited property can be complex, and it’s often wise to consult with a tax professional or financial advisor. They can provide personalized advice based on your situation and help you explore all possible tax strategies. For instance, if you’re contemplating selling an inherited property, timing can be crucial, and a professional can guide you on the most tax-efficient approach.

Final Thoughts

Inheriting property comes with a mix of emotions and financial considerations, with taxes playing a significant role. While the prospect of paying capital gains tax on an inherited property might seem daunting, the rules around the stepped-up basis generally work in your favor, potentially reducing the amount you owe. Armed with this knowledge and the guidance of a professional, you can navigate the tax implications of your inheritance with confidence.

Still Wondering?

If you’ve got more questions or you’re looking for specific advice tailored to your situation, reaching out to a tax professional is your next best step. Remember, when it comes to taxes, it’s not just about what you owe; it’s also about understanding your rights and the opportunities to minimize your tax burden legally and effectively.

Inheriting property is a journey through a complex landscape of emotions and financial decisions. With the right information and professional guidance, you can make informed choices that honor the legacy left to you while ensuring you’re in good standing with tax laws.

Do You Pay Capital Gains Tax on Inherited Property?