The most commonly used scoring tool used by mortgage lenders is the FICO Credit Score. If you’re thinking of purchasing a home, it’s important that you understand what the scoring system is and how it can affect your ability to obtain a loan. We recommend you take a few minutes to read through this blog post and familiarize yourself with the elements of the FICO Credit Score and the suggested tips for improving yours.

What Is the FICO Credit Score?

The FICO Credit Score is calculated by the Fair Isaac Corporation, which is a company that specializes in predictive analytics. You’ll often see the name alongside the major credit reporting companies – Equifax, Experian or TransUnion – but it’s important to know that it alone does not handle credit recordkeeping. It takes the information it analyzes from the top three credit reporting companies.

What is the FICO Credit Score comprised of?

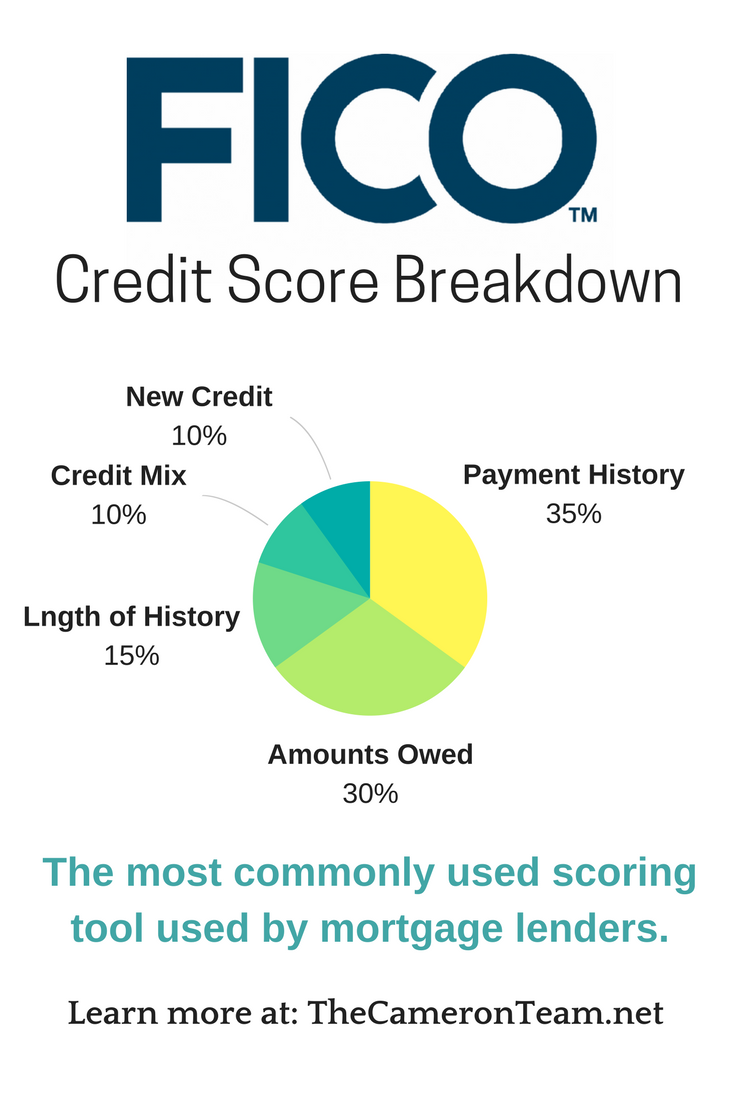

The FICO Credit Score is comprised of multiple pieces of information from your credit history. It analyzes both good and bad factors, so while one piece may lower the score, another can help raise it up. All of these factors are listed in the graph below. The percentage represents how much weight a collection of information has when calculating the total score.

This graph is a representation for the general population. Each score is calculated a little differently for each person depending on their overall credit history. For example, a person with a long credit history will be calculated differently than someone with a short credit history.

What isn’t in the FICO Credit Score?

Thanks to the Consumer Credit Protection Act, the FICO Credit Score does not consider your race, color, religion, national origin, sex and marital status. It doesn’t consider your age, location, child/family support, salary, occupation, or employment information. Though that doesn’t mean the lender won’t. Interest rates, credit counseling, certain soft-pull credit inquiries, and any information not included in your credit history are also not considered.

How Do I Improve My FICO Credit Score?

First, check your credit report for inaccuracies. You can do this for free through websites like Credit Karma without affecting your credit score. Credit Karma will explain the best route for removing inaccurate information from your credit report. Some companies allow you to submit changes through Credit Karma, others require you to contact them directly.

Here are some category-specific tips, as well:

1. Payment History – If you aren’t current, get current. Make your credit payments on time and consistently. This is the biggest factor in the FICO Credit Score. Setting up payment reminders or auto-pay will help greatly.

2. Amounts Owed – Pay down your debt, don’t just move it around by using one credit card to pay off another. When you pay off an account, don’t close it down as this may negatively affect the score. Closing an account does not make it go away and it may still be considered in the calculations.

3. Length of Credit History – The longer the appropriately managed credit history the better. If you’re brand new to managing credit, don’t open a bunch of new credit cards, because that will shorten the average account age and make you look risky.

4. Types of Credit – Have a good mix of credit history. Try to include installment loans and credit cards, but only open accounts as needed. Be choosy.

5. New Credit – Shop around for the best rate and do it within a short period of time (3 days to 1 week). This will limit the effect it has on your credit score as the credit inquiries in that small timeframe will be identified as shopping for one loan and not many.

The sooner you get to work on improving your credit history the better. Trying to make changes after you’ve already been approved for financing can be detrimental to your ability to secure final loan approval and history plays a large part in calculating your FICO Credit Score. For more information, visit myFico.

If you’re thinking of buying a home in the Wilmington area and would like to be put in touch with a reputable lender, give us a call at (910) 202-2546 or send us a message through our contact page. We’re happy to pass along some names of people we have worked with in the past and had good experiences with, including lenders who are happy to provide some direction on how to improve your credit score.

Related Posts

[the_grid name=”Home Buyer Tips”]